The Federal Home Loan Banks as Infrastructure for Shared Ownership

Eleven regional cooperative banks allocate billions for affordable housing through mandated programs — including community land trusts. A case study in how existing financial infrastructure can be steered toward stewardship models.

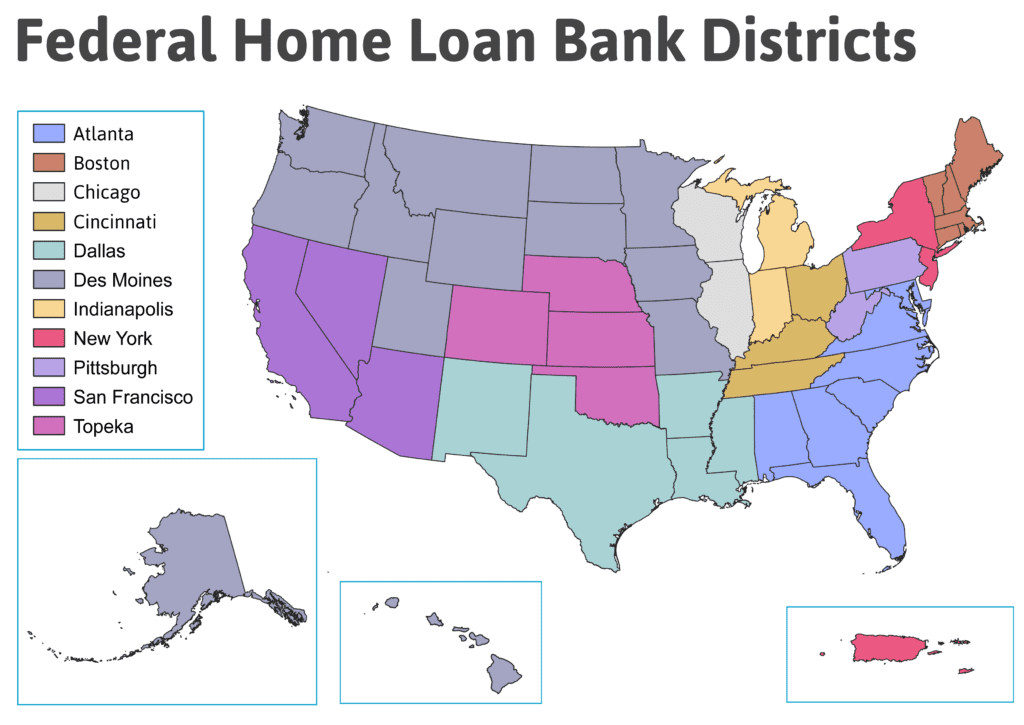

The Federal Home Loan Bank system — 11 regional cooperatives serving 6,500 member institutions — operates as a quiet but substantial piece of America’s housing finance infrastructure. As government-sponsored enterprises, these banks provide reduced-rate capital to credit unions, commercial banks, and community development financial institutions. Federal law requires each bank to allocate at least 10% of annual earnings to an Affordable Housing Program, funding that flows through member institutions to housing developers via competitive applications.

What makes this relevant to governance experimentation is how the system accommodates — and increasingly prioritizes — shared equity models like community land trusts. Four of the eleven banks now explicitly reference CLTs in their scoring criteria, recognizing permanent affordability mechanisms as distinct from conventional homeownership subsidies. The structural fit is notable: 95% of shared equity programs serve households at or below 80% of area median income, precisely the threshold mandated by statute. These aren’t grants shaped to fit an agenda; they’re an existing allocation mechanism being steered toward stewardship.

The application process remains cumbersome — nonprofits must partner with member financial institutions, navigate annual deadlines that mostly open in May, and compete within frameworks established by each bank’s advisory council. But the flexibility built into the system allows regional adaptation. Banks in Boston and Pittsburgh have adjusted their criteria to improve scores for permanent affordability models, a small procedural shift with material consequences for which ownership structures get built.

This is infrastructure work: not designing new systems from scratch, but identifying leverage points within existing ones. The Home Loan Banks aren’t experimental governance in any flashy sense. They’re 93-year-old cooperative financial institutions with statutory obligations. But their capacity to fund land trusts — models that separate ownership from stewardship, that prioritize use rights over speculative value — suggests how legacy systems might be reconfigured toward relational rather than extractive ends.